This is the next part of my AIM IT Project. Here is the homepage of the project where you can find links to the previous posts, and you can monitor the performance so far in the live spreadsheet.

What I am looking for in these companies is not so much a long term investment, but a special situation, some overlooked asset held on the balance sheet that alone is worth more than the market cap.

Amphion Innovations (AIM:AMP)

A new day and another horrible looking chart of shareholder value destruction to start us off. I should say that not all Investment Trusts on AIM destroy shareholder value, but I’ve been starting with the most heavily discounted to NAV so its no surprise these are the worst performers.

Amphion work closely with a number of partner companies in the technology sector. They provide operational guidance as well as funding and then assistance in raising additional capital through the equity markets while these partners develop their intellectual property (IP) into a marketable and profitable business. The latest annual report lists all these companies from page 5.

The board seems to have little experience in the investment world, and most come from backgrounds in technology companies or pharmaceuticals. The board takes home around $1m a year, very high for a company with net assets of only $17.6m. The total administrative expenses of the fund (including salaries) averages about $2m a year.

The IP they hold is hard to value, so NAV isn’t the best measure of intrinsic value. Naturally, the board thinks the IP value is well in excess of NAV but in the absense of anything concrete, here is the performance of NAV over the last few years.

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 (H1) | |

| NAV per share (p) | 30 | 26 | 14 | 13 | 9 | 8 |

They did actually manage some NAV increases in the early years, but that is easy when you are constantly issuing shares at a premium. The share price today is 3.9p, roughly 50% of NAV.

This company is virtually impossible to accurately value, and in my opinion it is purely speculative to invest in such early stage technology and pharma companies.

Share Price: 3.89p

NAV per share: 8.0p

Valuation: –

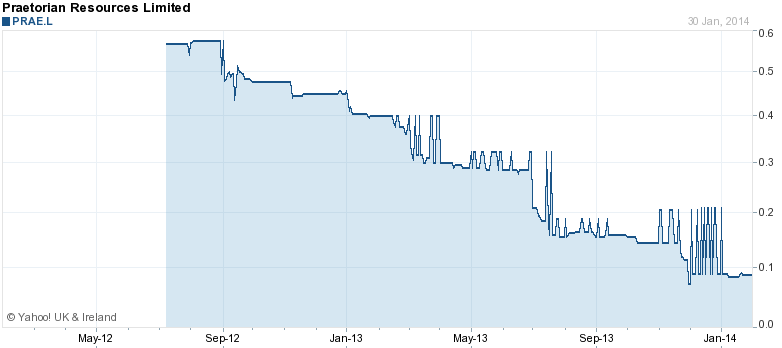

Praetorian Resources (AIM:PRAE)

As the name may suggest, PRAE invests in resource and commodity companies. It is fairly young, being listed on AIM in 2012 in order to take advantage of what they saw as “indiscriminate sell offs” in resource equities. Here is its admission document which gives details of the strategy. Its core investments are listed on this webpage, and are all listed on stock exchanges which makes valuation much easier for me.

The investment manager has also managed Arlington Special Situations Fund which I have so far been unsuccessful in finding the performance of. He ran it for 5 years though so I think it is safe to say that if it had been stellar performance he wouldn’t now be managing a small £10m fund. The funds expenses are quite low, at £300k a year but many directors have deferred or waived their fees temporarily, costs would normaly be circa £500k.

Reading through the managements reports on the performance of each period, I get the impression they expected stock prices to rebound simply because they had fallen. They give no mention of how the companies they are invested in are doing and continually focus on investor sentiment and how people are “ignoring” the resource sector.

I took a look at some of their holdings, which are concentrated into 6 positions. One of these is Besra Gold which despite the collapse in gold prices, still generates positive cash flows. Unfortunately these are reinvested in the business for exploration and development. Only an upturn in the gold price will save this company, not something I want to bet my money on.

Another company they have a stake in is Equatorial Palm Oil (AIM:EPO), a company with no revenue and losing money. Even mature palm oil companies barely make any returns on their assets, I don’t see the appeal in this. If these are the best companies they can pick out of a distressed market then I despair.

Maybe one of these companies will come good, but all are high risk so I’ll only give a token valuation to the portfolio.

Share Price: 8.75p

NAV: 18.1p

Valuation: 2p

Upside: (77%)

Skil Ports & Logistics (AIM:SPL)

Skil is a very simple company in terms of balance sheet, it is made up almost entirely of cash, meaning that its Price/Book ratio of 0.42 shows it is trading at a discount to net cash. You might consider it a no brainer then, companies with negative enterprise value have been shown to produce outsized returns in the long run.

But there is more to this story, companies don’t trade at a discount to net cash for no reason, even if they are small illiquid stocks. SPL is an investment vehicle looking to build a port and logistics centre in India. Its chairman is Nikhil Ghandi who has a history of successfully building similar projects in India.

The company was listed on AIM in 2010 and was meant to be completed and revenue producing by 2014. Obviously this hasn’t happened and as at the last news release, they still had a large cash pile yet to invest in the infrastructure. The delays where caused by regulatory considerations which have now been resolved. The companies admission document details the project plans, which is planned to cost roughly £110m, funded by current cash of £65m and debt of £45m. Costs are still said to be within budget but given management said that the regulatory delays wouldn’t affect the planned time-frame until it was obvious it would be missed (completion is now delayed until September 2015), I wouldn’t put too much faith in that. I think to be conservative the final project could cost £150m and leave the company with debt of £85m.

So this investment isn’t without its risks. Things are made worse by the fact the company hasn’t given a market update since September, when it announced construction would start and it would provide “regular updates”. The company was trading below net cash then, but we don’t know what the situation is now.

Another risk is the integrity of management. The admission document says this

“The SKIL Group, like many of its peers and other organisations doing business in India, is susceptible to disputes with commercial counter-parties and local regulators, which often include allegations of criminal as well as civil wrong doing. The Directors believe that such claims, and any ensuing litigation, are part of the ordinary course of business for many companies in India. The SKIL Group, its ultimate controlling shareholders (including Mr. Nikhil Gandhi) and its directors are currently engaged in a number of both criminal and civil proceedings, at different levels of adjudication before various courts, tribunals and enquiry officers in India, all of which are being contested. These matters are:

- criminal proceedings which name Mr. Gandhi, among others, and include allegations of forgery of bills, fraudulent evasion of customs duties and dishonouring of cheques;

- preliminary investigations by SEBI into price movements of equity shares and transactions in equity shares of companies in which Mr. Gandhi holds directorships or controlling interests;

- and an order of SEBI against a director and certain officers of SKIL Group companies (which does not include Mr. Nikhil Gandhi) relating to allegations of insider dealing”

So it appears the chairman may have been involved in some tax evasion.

But I can’t help be compelled by this company when it trades so far below its net cash position and is building a new port in a growing part of the world. I have seen some very blue sky projections of this project producing annual EBITDA of £50m once fully operational, which for a company with a market cap of £25m seems like a lot of upside.

I never trust blue sky thinking though, for me the primary consideration has to be is this investment protected by the cash on the balance sheet, or whatever that cash will be spent on. Given the Chairman’s history of building successful and profitable projects in India I don’t think the money will be wasted and he clearly has companies with the financial resource to finish this project if they have difficulty raising debt.

I will need a little more thought on this, but for now I think this company is worth book value. If I do end up buying that valuation will likely drastically change based on the operational updates of the company.

Share Price: 57.5p

NAV: 140p

Valuation: 140p

Upside: 143%

Disclosure: AMP, PRAE – no position, SPL – may initiate position

Investing Sidekick

Founder of Investing Sidekick. Works as a research analyst and is an avid value investor, always searching for undervalued shares.

Keep it up, man! You’ll get to the good stuff in due course… 😉

Thanks will do. I’m sure I’ll find one company that hasn’t been a horrible long term investment :p

A good write up on SPL on the MF boards

http://boards.fool.co.uk/ski-skil-and-skillspl-12991655.aspx